If you have been watching the Monterey Peninsula real estate market with any regularity, you have likely noticed something that the raw listing count does not fully explain: fewer homes are actually changing hands. Sales volume — the number of transactions that close each month — remains well below the historical averages that defined this market through much of the last decade. Understanding why requires looking past surface-level inventory numbers and examining the structural forces that are quietly reshaping how this market operates.

If you have been watching the Monterey Peninsula real estate market with any regularity, you have likely noticed something that the raw listing count does not fully explain: fewer homes are actually changing hands. Sales volume — the number of transactions that close each month — remains well below the historical averages that defined this market through much of the last decade. Understanding why requires looking past surface-level inventory numbers and examining the structural forces that are quietly reshaping how this market operates.

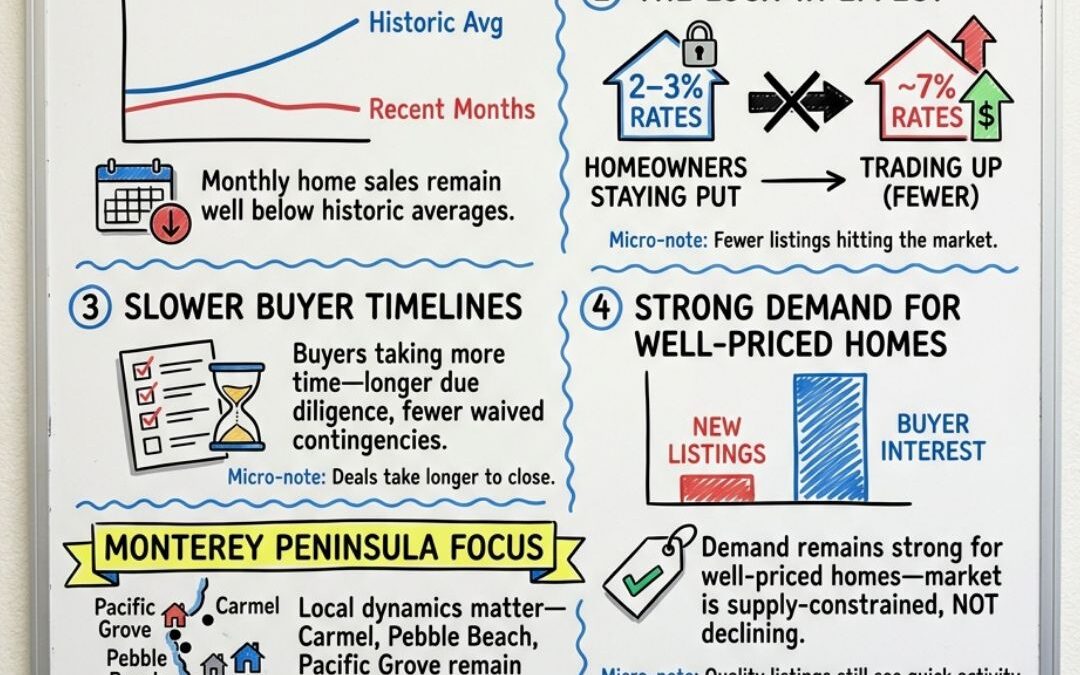

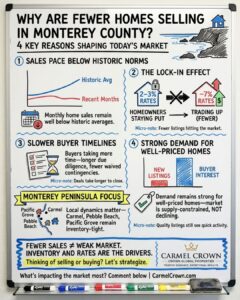

Transaction Volume Has Declined — and That Is Not the Whole Story

Monthly closed sales across Monterey County have trended meaningfully below the pace recorded in prior years, a pattern that mirrors national data but carries distinct local texture. Nationally, existing home sales have run at annualized rates not seen since the mid-2000s on the low end. On the Monterey Peninsula specifically, the combination of elevated prices, constrained supply, and a cautious buyer pool has compressed transaction activity in ways that are worth unpacking carefully.

The instinct is often to read low transaction volume as a sign of a weakening market. That interpretation is incomplete here. A market with fewer sales but stable or rising prices is not a declining market — it is a supply-constrained one. The distinction matters, particularly for homeowners who may be contemplating whether now is a reasonable time to sell, and for buyers trying to gauge whether they are walking into a market that is softening or simply moving more slowly.

The Lock-In Effect: Why So Many Homeowners Are Staying Put

The dominant structural force behind low transaction volume right now is what economists and housing analysts have come to call the “lock-in effect.” The mechanics are straightforward: a large share of existing homeowners in Monterey County — and across California broadly — secured fixed-rate mortgages in 2020 and 2021 when the 30-year rate sat between 2.65% and 3.25%. Those loans are now attached to those homes. Selling means giving them up.

For a homeowner carrying a $1.2 million mortgage at 2.875%, the monthly principal and interest payment is approximately $4,980. If that same homeowner sells, moves, and finances a comparable property at today’s prevailing rate — which has hovered near 6.75% to 7.0% for most of the past year — that payment rises to roughly $7,800 or more for the same loan amount. That is a monthly cost increase exceeding $2,800, or more than $33,000 per year, simply from the rate differential.

The financial calculus is not subtle. Many homeowners who would otherwise consider upsizing, downsizing, or relocating have concluded that the numbers do not support a move — not yet. This decision, multiplied across thousands of homeowners on the Peninsula and throughout the county, is the single largest contributor to compressed listing inventory and, by extension, suppressed transaction volume.

This is not irrational behavior. It is rational economic self-interest, and it will likely persist until either mortgage rates decline meaningfully, the homeowner’s personal or financial circumstances create sufficient motivation to move regardless of rate, or enough time passes that the psychological anchor of the prior rate loses its grip.

Buyers Are Moving More Deliberately

On the demand side, buyers have not disappeared — but the pace at which they move from inquiry to offer to contract has lengthened considerably. This is a behavioral shift as much as a financial one.

In the accelerated market conditions of 2020 through early 2022, buyers regularly waived contingencies, submitted offers sight unseen, and competed in escalating bid situations where speed was rewarded above deliberation. That environment has largely passed. Today’s buyers — many of whom are purchasing at price points that represent a significant share of their net worth or retirement assets — are conducting more thorough due diligence, taking additional time to evaluate neighborhoods, and often waiting to see whether a property they have identified might experience a price adjustment before committing.

This extended decision timeline does not indicate a lack of conviction. In many cases, it indicates the opposite: buyers who are serious enough about the investment to get it right. For sellers and their advisors, understanding this shift is consequential. A property that receives measured interest over several weeks from qualified buyers is behaving differently than properties in the 2021 market — but it is not necessarily underperforming the current environment.

Demand Remains — For the Right Properties

One of the most consistent patterns observable across the Monterey Peninsula market right now is the bifurcation between well-priced properties and those that enter the market carrying optimistic assumptions. Homes priced with a clear-eyed understanding of current comparable sales data are still moving. Days on market for this segment remains reasonable. Multiple-offer situations, while less common than in prior years, still occur when a property is positioned correctly.

The market has not lost its appetite for quality. What it has lost is its tolerance for price discovery — the practice of listing above market to see what happens. Buyers are well-informed, have ample time to research recent sales, and are working with advisors who understand local conditions. An overpriced listing does not generate negotiation; it generates indifference.

Demand on the Peninsula is further supported by its fundamental attributes. The Monterey Peninsula is not a market driven primarily by employment migration or speculative appreciation cycles. Its buyer pool includes second-home purchasers, retirees relocating from higher-cost metros, investors seeking vacation rental income in one of California’s most recognized leisure destinations, and a consistent international buyer segment attracted to the lifestyle and relative stability of coastal California real estate. These motivations do not evaporate because mortgage rates are elevated. They extend timelines.

What This Means if You Are Considering a Move

For homeowners evaluating whether to sell: the lock-in effect is real, and the financial analysis it prompts is worth taking seriously. That said, life circumstances — estate transitions, family changes, retirement relocation, or the need to access equity — often create valid reasons to move regardless of where rates sit. The question is not only “Is this the ideal market?” but “Does waiting serve my personal and financial goals?”

For buyers currently active in the market: the slower pace is a structural feature, not a temporary lull. Approach it with patience and precision. Properties that represent genuine value within their micro-market — Carmel-by-the-Sea, Pebble Beach, Pacific Grove, Monterey, Carmel Valley — are not accumulating on the market waiting to be discovered at a discount. They are selling to buyers who have done the work.

For investors: compressed transaction volume in a market with strong underlying demand is not a signal to exit. It is a signal to evaluate the market’s long-term supply constraints and the durability of rental demand in a region where new construction remains limited by geography, regulation, and community character.

A Market Worth Understanding Carefully

The Monterey Peninsula real estate market is not broken. It is operating under a specific set of structural pressures — the lock-in effect, deliberate buyer behavior, and the natural recalibration that follows an exceptional period of low-rate activity — that have reduced transaction volume without undermining the market’s fundamental stability.

Navigating this environment well requires local expertise, current data, and a clear-eyed read on what is actually happening versus what the national headlines suggest. The team at Carmel Crown and Crown Global Properties works exclusively in this market, with deep familiarity across the Peninsula’s distinct neighborhoods and price segments. If you are weighing a decision — whether to sell, buy, or invest — we are available to provide a grounded, no-pressure consultation based on current conditions.

What do you think has had the biggest impact on today’s market: mortgage rates, affordability, or something else? We would be glad to hear your perspective in the comments below.